June international passenger demand rose 5.5% compared to the same month last year, with airlines in all regions except Africa recording growth and the strongest gains among Middle East carriers. Capacity climbed 5.7% and load factor dipped 0.2 percentage points to 81.4%.

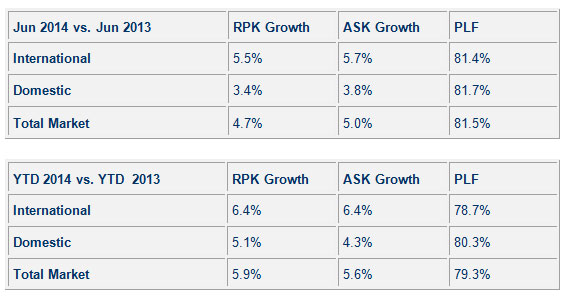

GENEVA – The International Air Transport Association (IATA) announced global passenger traffic results for June showing a modest deceleration in demand growth compared to the prior month. Total revenue passenger kilometers (RPKs) rose 4.7% over the year-ago period, which was below the 6.2% year-on-year increase recorded in May 2014. June capacity (available seat kilometers or ASKs) increased by 5.0%, causing load factor to slip 0.2 percentage points to 81.5%.

GENEVA – The International Air Transport Association (IATA) announced global passenger traffic results for June showing a modest deceleration in demand growth compared to the prior month. Total revenue passenger kilometers (RPKs) rose 4.7% over the year-ago period, which was below the 6.2% year-on-year increase recorded in May 2014. June capacity (available seat kilometers or ASKs) increased by 5.0%, causing load factor to slip 0.2 percentage points to 81.5%.

“June traffic growth at 4.7% is encouraging even though it is a slight weakening on May’s performance. Earlier signs of a softening in demand are dissipating. While that’s good news there are many risks in the political and economic environment that need careful monitoring,” said Tony Tyler, IATA’s Director General and CEO.

International Passenger Markets

International Passenger Markets

June international passenger demand rose 5.5% compared to the same month last year, with airlines in all regions except Africa recording growth and the strongest gains among Middle East carriers. Capacity climbed 5.7% and load factor dipped 0.2 percentage points to 81.4%.

- European carriers saw demand increase 5.6% in June versus June 2013. This is consistent with steady and continued economic recovery for the region. Capacity rose 5.3% and load factor climbed 0.3 percentage points to 83.8%.

- Asia-Pacific carriers’ traffic rose 4.9% compared to the year-ago period but capacity rose 6.7% and load factor slipped 1.3 percentage points to 77.9%. The outlook for this region looks broadly positive, with measures of manufacturing activity and export orders pointing to better performance of China.

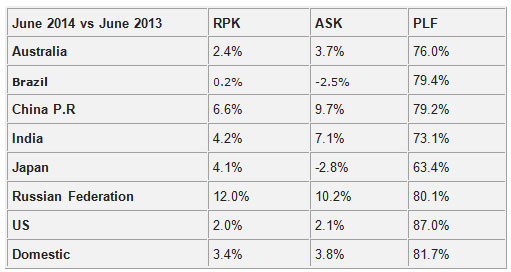

- North American airlines experienced a 3.1% rise in traffic compared to June a year ago. Capacity rose 5.9%, however, which caused load factor to fall 2.2 percentage points to 85.1%, which still was the highest among the regions. Recent data from the US suggest that underlying growth trends in business activity are positive and the unemployment rate is showing improvement.

- Middle East carriers’ demand jumped 10.8% in June, the largest increase for any region and reflecting the continued strength of regional economies and solid growth in business-related premium travel. Capacity climbed just 5.9%, propelling load factor up 3.7 percentage points to 82.1%.

- Latin American airlines’ traffic rose 7.1% compared to June 2013. Capacity rose 6.6% and load factor climbed 0.4 percentage points to 79.5%. While growth was solid, it was below the 8.1% annual result for 2013. Part of the softness is owing to a significant reduction in capacity this year compared to last as well as sluggishness in major economies and consequently, regional trade growth.

- African airlines saw a 2.7% reduction in demand in June, while capacity climbed 2.0%, resulting in a 3.3 percentage point drop in load factor to 67.3%, the lowest load factor for any region. The weakness could be attributable to adverse economic developments in some parts of the continent, including the slowdown of the major economy of South Africa.

Domestic Passenger Markets

Domestic travel demand rose 3.4% in June compared to June 2013, with the strongest growth occurring in Russia and China. Total domestic capacity was up 3.8%, and load factor slid 0.3 percentage points to 81.7%.

- Russian domestic demand rose 12% in line with government economic policies that support expansion in domestic air travel.

- Brazil domestic demand, by contrast, experienced virtually zero demand growth in June compared to June 2013, despite being the host of the FIFA World Cup. Conditions in the Brazilian economy have done little to boost growth in air travel this year, with inflation continuing to rise and consumer confidence on the wane.

The Bottom Line

“Demand for air travel and the connectivity it provides remains strong. But uncertainty in the global political and economic climate has the potential to negatively impact demand. Risk is today’s reality, whether it’s conflict in the Middle East, sanctions and an impending trade war with Russia, possible default in Argentina or the Ebola outbreak in Western Africa. All have the potential to dent demand. We are optimistic that the industry will still end the year with an improvement in profitability over 2013. But the regional impact of some of these risks will challenge some airlines more than others,” said Tyler.

“One of the biggest regional challenges could be Ebola. Travelers should be reassured that airlines are coordinating closely with the World Health Organization (WHO) and the International Civil Aviation Organization (ICAO). WHO currently advises that the risk to travelers is low and is not recommending travel restrictions or border closings. If, however, a passenger feels unwell it is always advised that they seek the advice of a doctor before traveling,” said Tyler.

“The aviation community has worked with WHO and ICAO in several challenging public health situations during recent years. As a result, guidance and procedures have been developed to keep travel safe. These include procedures for front line staff to detect those potentially infected and handle them appropriately. IATA continues to work with WHO and ICAO to ensure that airlines are well-prepared to deal with the situation however it unfolds,” said Tyler.